Public Adjusters are one of the insurance industries best kept secrets.

They're your advocate!

They're your advocate!

Why hire a Public Adjuster (PA)?

- As a public adjuster, our primary focus is on representing your interests and helping you secure the maximum settlement possible for your insurance claim. We do this by:

- Working exclusively for you, and never for the insurance company. Your interests always come first, and we are dedicated to ensuring that your claim is handled fairly and in accordance with the terms of your policy.

- Familiarizing ourselves with your insurance policy and its coverages. We have a thorough understanding of the different types of coverage that may be available to you, and we can help identify which coverages apply to your claim.

- Conducting a thorough inspection, research, and estimate of your damages. This includes identifying all of the damages to your property and personal belongings, and providing the insurance company with a detailed and accurate estimate of the cost to repair or rebuild your property.

- Negotiating with the insurance company on your behalf to secure a fair and timely settlement. We have the knowledge and expertise to advocate for you and negotiate a settlement that meets your needs.

- Working on a variety of claims, including denied claims, underpaid claims, existing claims, new claims, and supplement claims. We can even help you reopen a claim if it has been previously denied or settled.

- Operating on a contingency basis, which means that we only get paid if you do. Our fees are typically a percentage of the settlement we are able to secure for you, so you can be confident that we are motivated to work hard on your behalf.

|

|

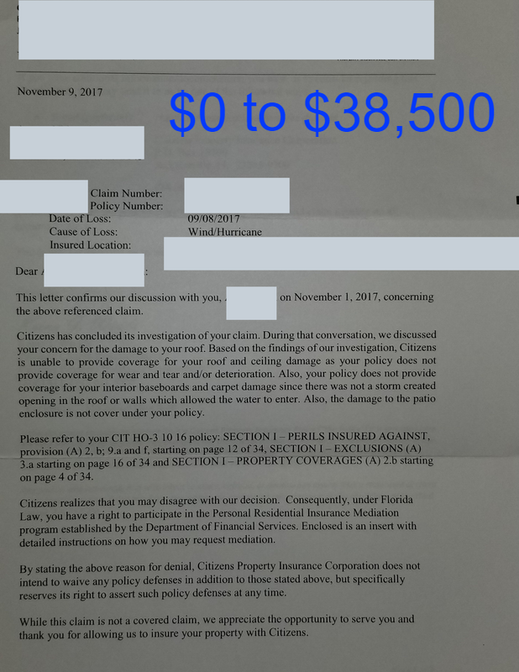

Denied Claim? |

State Licensed and Bonded Public Adjuster

W112859

W112859

Insurance Company...

|

|

|

|

Insurance Company...

|

|

Insurance Company...

|

Insurance Company...

|

|

Public Adjuster's basic steps to handling a claim

Here are the steps we typically follow when working on an insurance claim:

- Investigate the loss: We will carefully examine the damages that have occurred to your property, as well as any personal possessions or other contents that may have been affected. This includes identifying all of the damages and documenting them thoroughly.

- Review your insurance policy: We will carefully review your insurance policy to determine which coverages apply to your claim. This helps us ensure that your claim is handled in accordance with the terms of your policy.

- Document the loss: We will prepare a detailed and accurate estimate of the damages, including photographs and other documentation as needed. This is important because it helps to trigger the policy coverages and establishes the extent of the damages for the insurance company.

- Present the insurance claim: We will work with you to prepare and submit the insurance claim to the insurance company. This includes providing all of the necessary documentation and answering any questions that the insurance adjuster may have.

- Review and negotiate the claim: We will review the insurance company's initial settlement offer and negotiate on your behalf to ensure that you receive a fair and timely settlement.

- Settle the claim: Once the claim has been settled, we will work with you to ensure that you receive the settlement payment in a timely manner.

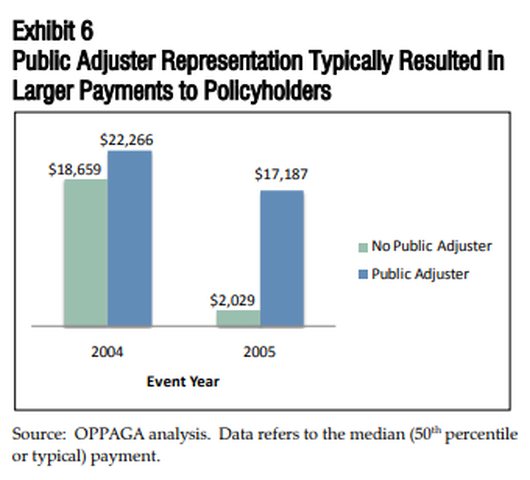

A 3rd Party study shows the benefit of hiring a Public Adjuster.

Click on the graph for the full report done by OPPAGA on PA's with Citizens Claims

No Recovery, No Fee

Only pay, if you get PAID.

Only pay, if you get PAID.

We will review your policy and inspect any claim related damage.

We have extensive experience working with a wide range of claim types. Some of the most common types of claims we handle include:

- Fire damage: If your home or business has suffered damages due to a fire, we can help you navigate the insurance claims process and ensure that you receive the maximum settlement possible to cover the cost of repairing or rebuilding your property.

- Smoke damage: Smoke damage can occur as a result of a fire, but it can also be caused by other factors such as faulty appliances or malfunctioning HVAC systems. We can help you identify the cause of the smoke damage and ensure that your claim is handled fairly and in accordance with the terms of your insurance policy.

- Water damage: Water damage can be caused by a variety of factors, including broken pipes, leaky roofs, failed appliances, and malfunctioning air conditioning systems. We have experience dealing with all types of water damage claims, and we can help you identify the cause of the damage and ensure that your claim is handled effectively.

- Wind damage: Wind damage can occur as a result of severe storms, hurricanes, or other weather-related events. We can help you identify the extent of the damages and provide the insurance company with a detailed and accurate estimate of the cost to repair or rebuild your property.

- Storm damage: Storms can cause a wide range of damages to your home or business, including wind damage, water damage, and structural damage. We have experience dealing with all types of storm damage claims, and we can help you navigate the insurance claims process and secure the maximum settlement possible.

- Other types of claims: In addition to the claims listed above, we have experience working with a wide range of other claim types, including vandalism, and other types of property damage. Regardless of the cause of the damages, we are here to help you navigate the claims process and ensure that you receive the maximum settlement possible.

Public Adjusters are experts on your side

Questions Frequently Asked

1 - What knowledge does a Public Adjuster offer that will help me with my insurance claim?

A Public Adjuster is an expert with insurance policies and protocols. Think of a Public Adjuster as your personal insurance claims specialist, your insurance professional. Having experience with many different policies and situations gives us insights often overlooked by the policyholder and many other professionals. There many steps and timelines that need to be kept and ways to expediate the process. Depending on the claim there may be a need to bring on other specialty professionals - engineers, contractors, accountants, lawyers, etc.

2 - Public Adjusters are one of the reasons for insurance premium increases?

A PA should never take a claim that is not supported by your insurance coverages at the time of loss. There are PA's that will sling mud to the wall to see what sticks. A good PA will investigate the loss, review policy coverages, and determine if the policy supports filing a claim. There are times when the claim is black and white per the policy, but the insurance company's representatives insist it is not ( this contributes to premium increases). When there is a dispute over policy language, it's time to hire a lawyer. People file unwarranted claims, unfortunately (contributing to premium increases). Insurance policies are thought of as maintenance contracts by some policyholders, which there are not ( contributing to premium increases).

3 - How does a PA get paid and how much does it cost to hire a Public Adjuster?

Most PA's take a percentage of the claim they helped settle. A variety of things can determine the amount charged, complexity, reopened claim, new claim, are experts needed, type of claim (Hurricane, Fire, Water Damage, Flood, etc.), expertise of the PA, and other factors. Typically 10%-20% is the percentage charged, and additional fees can be part of the agreement if experts or additional expenses are needed. When the Governor's office declares a state of emergency, a PA's fee is capped to 10%. All other times the max a PA can charge is 20%.

4 - Should I hire a Public Adjuster or Lawyer?

A PA should never tell you not to hire a lawyer. The policyholder is the only one to decide—the difference between hiring a PA and a lawyer. The moment the PA is hired, the file should be put together as if a lawyer will be hired to finish the claim. A PA cannot argue policy language. Only a lawyer can. The PA can point to the policy section that covers the loss and provide all the supporting documentation to the claim. Some lawyers hire a PA when they receive a claim from a client. The PA is hired because they are experts at applying policy coverages to the damage from the loss. Most contractors don't have a clue about how to do so. Contractors are great at building and fixing damaged property.

5 - My contractor, roofer, or restoration/remediation company say they work with the insurance, and I don't need a PA or lawyer?***

A lot of contractors ( all the above included) say (advertise) they work with insurance companies on your behalf (do they really?). First, they are not allowed to negotiate with your insurance company. Providing the insurance company with an estimate and explaining the assessment is all a contractor is entitled to do per state statute (included below). A PA is the only one (besides a lawyer) allowed to negotiate an insurance claim. Now here is the real world, a contractor wants you to sign their contract entitling them to your insurance benefits for work they will perform. The agreement more than likely says, If they don't get paid from the insurance company, the policyholder is responsible for the invoice. Meaning you pay the invoice, or a lien can be placed on your property, or a lawsuit can be filed against the policy holder or the insurance company. By signing their work authorization, you're giving the authority to take any of the previously mentioned actions. They are some great companies out there willing to do right by you and do outstanding work. Some of these contractors can give peace of mind when you're in the midst of the chaos. Be careful whom you hire and what you sign.

6 - Should I hire a PA or a Contractor?

9 out of 10 times, I would suggest hiring a PA. A PA's goal is to get you the money, so you can decide how to have the work done. When the PA helps you get the correct settlement, you can choose to hire a general contractor, sub-contractors, or do some of the repairs yourself. When you hire a contractor that bills your insurance company directly, all the money goes to them. On some claims, their profit margins are outrageous. The policyholder is the one who pays for the insurance premiums. It's their money to decide how repairs are to be made.

7 - Can the Contractor / PA act as both on my claim?

No. The Contractor / PA has to be one or the other. It is a conflict of interest to act as both on a claim.

8 - How can a PA get increased claim payout or a denied claim paid?

An insurance policy has multiple coverages within its pages. Some examples would be contents coverage, law and ordinance, mold, and emergency repairs, not to mention additional riders that could have been purchased. Each policy is unique to the policyholder and their needs and should be read through to determine what coverages are available. Properly documenting and presenting a claim is how payments are increased and denials turned in paid claims.

9 - I've heard Public Adjusters overinflate claims?

Unfortunately, there are some Public Adjusters that will do so. People are also posing a PA ( it's a big issue). Some Public Adjusters believe it's a negotiation tactic, but it's not. It only delays the process and causes frustration for all parties involved. We don't overinflate claims. When a claim is handled according to the policy and a thorough job is done by the PA, it cuts down on the hassle and time you receive a settlement. Here's food for thought: "If an insurance claim was inflated, why would the insurance company pay it? They don't!". Some PA's are good at policy, codes, state statutes, and documentation.

10 - Should I hire a Public Adjuster right away or wait?

It depends on the type of claim. If your claim seems black and white, reach out to your insurance company. Allow them to take care of you. If you feel the claim was not properly handled/paid, hire a public adjuster. Your claim was denied. Consult a public adjuster. If your claim was underpaid, consult a public adjuster. If you don't have the time to give the claim attention, hire a public adjuster. If you don't want to be bothered, hire a public adjuster. If your claim is questionable, consult a Public Adjuster.

www.leg.state.fl.us/statutes/index.cfm?App_mode=Display_Statute&URL=0600-0699/0626/Sections/0626.854.html

***626.854 “Public adjuster” defined; prohibitions.--The Legislature finds that it is necessary for the protection of the public to regulate public insurance adjusters and to prevent the unauthorized practice of law.(1)

A “public adjuster” is any person, except a duly licensed attorney at law as exempted under s. 626.860, who, for money, commission, or any other thing of value, directly or indirectly prepares, completes, or files an insurance claim for an insured or third-party claimant or who, for money, commission, or any other thing of value, acts on behalf of, or aids an insured or third-party claimant in negotiating for or effecting the settlement of a claim or claims for loss or damage covered by an insurance contract or who advertises for employment as an adjuster of such claims. The term also includes any person who, for money, commission, or any other thing of value, directly or indirectly solicits, investigates, or adjusts such claims on behalf of a public adjuster, an insured, or a third-party claimant. The term does not include a person who photographs or inventories damaged personal property or business personal property or a person performing duties under another professional license, if such person does not otherwise solicit, adjust, investigate, or negotiate for or attempt to effect the settlement of a claim.

***(15) A licensed contractor under part I of chapter 489, or a subcontractor of such licensee, may not advertise, solicit, offer to handle, handle, or perform public adjuster services as provided in subsection (1) unless licensed and compliant as a public adjuster under this chapter. The prohibition against solicitation does not preclude a contractor from suggesting or otherwise recommending to a consumer that the consumer consider contacting his or her insurer to determine if the proposed repair is covered under the consumer’s insurance policy, except as it relates to solicitation prohibited in s. 489.147. In addition, the contractor may discuss or explain a bid for construction or repair of covered property with the residential property owner who has suffered loss or damage covered by a property insurance policy, or the insurer of such property, if the contractor is doing so for the usual and customary fees applicable to the work to be performed as stated in the contract between the contractor and the insured.

1 - What knowledge does a Public Adjuster offer that will help me with my insurance claim?

A Public Adjuster is an expert with insurance policies and protocols. Think of a Public Adjuster as your personal insurance claims specialist, your insurance professional. Having experience with many different policies and situations gives us insights often overlooked by the policyholder and many other professionals. There many steps and timelines that need to be kept and ways to expediate the process. Depending on the claim there may be a need to bring on other specialty professionals - engineers, contractors, accountants, lawyers, etc.

2 - Public Adjusters are one of the reasons for insurance premium increases?

A PA should never take a claim that is not supported by your insurance coverages at the time of loss. There are PA's that will sling mud to the wall to see what sticks. A good PA will investigate the loss, review policy coverages, and determine if the policy supports filing a claim. There are times when the claim is black and white per the policy, but the insurance company's representatives insist it is not ( this contributes to premium increases). When there is a dispute over policy language, it's time to hire a lawyer. People file unwarranted claims, unfortunately (contributing to premium increases). Insurance policies are thought of as maintenance contracts by some policyholders, which there are not ( contributing to premium increases).

3 - How does a PA get paid and how much does it cost to hire a Public Adjuster?

Most PA's take a percentage of the claim they helped settle. A variety of things can determine the amount charged, complexity, reopened claim, new claim, are experts needed, type of claim (Hurricane, Fire, Water Damage, Flood, etc.), expertise of the PA, and other factors. Typically 10%-20% is the percentage charged, and additional fees can be part of the agreement if experts or additional expenses are needed. When the Governor's office declares a state of emergency, a PA's fee is capped to 10%. All other times the max a PA can charge is 20%.

4 - Should I hire a Public Adjuster or Lawyer?

A PA should never tell you not to hire a lawyer. The policyholder is the only one to decide—the difference between hiring a PA and a lawyer. The moment the PA is hired, the file should be put together as if a lawyer will be hired to finish the claim. A PA cannot argue policy language. Only a lawyer can. The PA can point to the policy section that covers the loss and provide all the supporting documentation to the claim. Some lawyers hire a PA when they receive a claim from a client. The PA is hired because they are experts at applying policy coverages to the damage from the loss. Most contractors don't have a clue about how to do so. Contractors are great at building and fixing damaged property.

5 - My contractor, roofer, or restoration/remediation company say they work with the insurance, and I don't need a PA or lawyer?***

A lot of contractors ( all the above included) say (advertise) they work with insurance companies on your behalf (do they really?). First, they are not allowed to negotiate with your insurance company. Providing the insurance company with an estimate and explaining the assessment is all a contractor is entitled to do per state statute (included below). A PA is the only one (besides a lawyer) allowed to negotiate an insurance claim. Now here is the real world, a contractor wants you to sign their contract entitling them to your insurance benefits for work they will perform. The agreement more than likely says, If they don't get paid from the insurance company, the policyholder is responsible for the invoice. Meaning you pay the invoice, or a lien can be placed on your property, or a lawsuit can be filed against the policy holder or the insurance company. By signing their work authorization, you're giving the authority to take any of the previously mentioned actions. They are some great companies out there willing to do right by you and do outstanding work. Some of these contractors can give peace of mind when you're in the midst of the chaos. Be careful whom you hire and what you sign.

6 - Should I hire a PA or a Contractor?

9 out of 10 times, I would suggest hiring a PA. A PA's goal is to get you the money, so you can decide how to have the work done. When the PA helps you get the correct settlement, you can choose to hire a general contractor, sub-contractors, or do some of the repairs yourself. When you hire a contractor that bills your insurance company directly, all the money goes to them. On some claims, their profit margins are outrageous. The policyholder is the one who pays for the insurance premiums. It's their money to decide how repairs are to be made.

7 - Can the Contractor / PA act as both on my claim?

No. The Contractor / PA has to be one or the other. It is a conflict of interest to act as both on a claim.

8 - How can a PA get increased claim payout or a denied claim paid?

An insurance policy has multiple coverages within its pages. Some examples would be contents coverage, law and ordinance, mold, and emergency repairs, not to mention additional riders that could have been purchased. Each policy is unique to the policyholder and their needs and should be read through to determine what coverages are available. Properly documenting and presenting a claim is how payments are increased and denials turned in paid claims.

9 - I've heard Public Adjusters overinflate claims?

Unfortunately, there are some Public Adjusters that will do so. People are also posing a PA ( it's a big issue). Some Public Adjusters believe it's a negotiation tactic, but it's not. It only delays the process and causes frustration for all parties involved. We don't overinflate claims. When a claim is handled according to the policy and a thorough job is done by the PA, it cuts down on the hassle and time you receive a settlement. Here's food for thought: "If an insurance claim was inflated, why would the insurance company pay it? They don't!". Some PA's are good at policy, codes, state statutes, and documentation.

10 - Should I hire a Public Adjuster right away or wait?

It depends on the type of claim. If your claim seems black and white, reach out to your insurance company. Allow them to take care of you. If you feel the claim was not properly handled/paid, hire a public adjuster. Your claim was denied. Consult a public adjuster. If your claim was underpaid, consult a public adjuster. If you don't have the time to give the claim attention, hire a public adjuster. If you don't want to be bothered, hire a public adjuster. If your claim is questionable, consult a Public Adjuster.

www.leg.state.fl.us/statutes/index.cfm?App_mode=Display_Statute&URL=0600-0699/0626/Sections/0626.854.html

***626.854 “Public adjuster” defined; prohibitions.--The Legislature finds that it is necessary for the protection of the public to regulate public insurance adjusters and to prevent the unauthorized practice of law.(1)

A “public adjuster” is any person, except a duly licensed attorney at law as exempted under s. 626.860, who, for money, commission, or any other thing of value, directly or indirectly prepares, completes, or files an insurance claim for an insured or third-party claimant or who, for money, commission, or any other thing of value, acts on behalf of, or aids an insured or third-party claimant in negotiating for or effecting the settlement of a claim or claims for loss or damage covered by an insurance contract or who advertises for employment as an adjuster of such claims. The term also includes any person who, for money, commission, or any other thing of value, directly or indirectly solicits, investigates, or adjusts such claims on behalf of a public adjuster, an insured, or a third-party claimant. The term does not include a person who photographs or inventories damaged personal property or business personal property or a person performing duties under another professional license, if such person does not otherwise solicit, adjust, investigate, or negotiate for or attempt to effect the settlement of a claim.

***(15) A licensed contractor under part I of chapter 489, or a subcontractor of such licensee, may not advertise, solicit, offer to handle, handle, or perform public adjuster services as provided in subsection (1) unless licensed and compliant as a public adjuster under this chapter. The prohibition against solicitation does not preclude a contractor from suggesting or otherwise recommending to a consumer that the consumer consider contacting his or her insurer to determine if the proposed repair is covered under the consumer’s insurance policy, except as it relates to solicitation prohibited in s. 489.147. In addition, the contractor may discuss or explain a bid for construction or repair of covered property with the residential property owner who has suffered loss or damage covered by a property insurance policy, or the insurer of such property, if the contractor is doing so for the usual and customary fees applicable to the work to be performed as stated in the contract between the contractor and the insured.

Attention to detail makes the difference!

Proud Veteran of the U.S. Air Force and U.S. Army

PA - W112859

Proud Veteran of the U.S. Air Force and U.S. Army

PA - W112859

Our goal is to get you paid!